Demystifying the Appraisal Process in Insurance Claims.

Demystifying the claims process in insurance can be a daunting task, especially when it comes to the appraisal stage. Appraisal is a crucial step that determines the value of a claim and is often misunderstood by policyholders. In this comprehensive guide, we will break down the appraisal process in insurance claims, providing you with a clear understanding of how it works and what to expect.

The insurance appraisal process is a formal and objective evaluation of the value of a claim. It involves an independent appraiser assessing the damages or loss and determining the appropriate compensation. This process ensures fairness and accuracy in resolving disputes between policyholders and insurance companies.

During the appraisal process, both the policyholder and the insurance company appoint their own appraisers. These appraisers assess the damages and negotiate a resolution. If they cannot reach an agreement, a neutral third-party, known as an umpire, is brought in to make a final decision.

It is important to note that the appraisal process is not an opportunity to negotiate the coverage of the insurance policy. It is solely focused on determining the value of the claim. Understanding the appraisal process can help policyholders navigate this stage with confidence, ensuring a fair resolution to their insurance claim.

What is an Appraisal Process?

The appraisal process in insurance claims is a demystifying procedure used to determine the value of a property or the extent of damage incurred in an insurance claim. It involves an impartial assessment conducted by a qualified appraiser to settle disputes between policyholders and insurance companies.

During the appraisal process, the appraiser examines the property or damage, analyzes relevant documents, and may also consult with experts or other professionals. They consider various factors such as the property’s condition, market value, replacement cost, and depreciation. Based on this assessment, the appraiser calculates the appropriate amount for the claim and prepares a detailed report.

Both the policyholder and the insurance company each choose their own appraiser to represent their interests. If these two appraisers cannot reach a mutual agreement on the valuation, they select an impartial umpire. The appraisers and umpire then work together to reach a fair and unbiased settlement.

The appraisal process is typically conducted in a timely manner to ensure that the claim is resolved efficiently. It provides an efficient alternative to litigation, saving time and costs for all parties involved. The outcome of the appraisal process is usually binding, meaning that both the policyholder and the insurance company must adhere to the calculated value.

Overall, the appraisal process plays a crucial role in insurance claims by providing an objective and transparent method to determine the value of a property or the extent of damage. It helps ensure a fair settlement for both the policyholder and the insurance company.

Importance of Appraisal in Insurance Claims

Demystifying the process of insurance claims requires a thorough understanding of the appraisal process. When it comes to resolving disputes and determining the value of a claim, appraisal plays a crucial role.

Insurance claims can be complex, and disagreements often arise between policyholders and insurance companies regarding the amount to be paid for a loss. In such cases, appraisal provides an impartial and effective method for reaching a fair settlement.

An appraisal involves a neutral third party, known as an appraiser, who assesses the value of the loss and determines the appropriate compensation. This appraiser is chosen by both the policyholder and the insurance company and serves as the mediator in the claims process.

The appraisal process helps ensure that both parties are treated fairly and that disputes are resolved quickly. It provides an objective assessment of the damages, taking into account factors like pre-existing conditions and depreciation. By relying on the expertise of an appraiser, insurance claims can be evaluated accurately, leading to fair and equitable settlements.

Additionally, the appraisal process helps maintain transparency and trust in the insurance industry. It ensures that insurance companies fulfill their obligations to policyholders and honor the terms of their policies. By having an appraisal as part of the claims process, policyholders can have confidence that their losses will be fairly evaluated and compensated.

In conclusion, the appraisal process is of utmost importance in insurance claims. It serves as a vital tool in resolving disputes and determining the value of a loss. By demystifying the process and understanding its significance, policyholders can navigate the claims process with confidence, knowing that a fair and objective assessment will be made.

When is Appraisal Process Initiated?

In the insurance industry, the appraisal process is initiated when there is a dispute between the insurance company and the policyholder regarding the amount of loss or damage covered under the policy. This process is often used as a means of resolving disagreements and reaching a fair and impartial resolution.

Demystifying the appraisal process is crucial for both the insurance company and the policyholder. Understanding the steps involved can help both parties navigate through the process smoothly and efficiently.

The appraisal process typically begins when the policyholder submits a claim to the insurance company. The insurer then assesses the claim and determines the amount they believe to be the appropriate coverage under the policy. If the policyholder disagrees with the insurer’s assessment, they can request an appraisal to resolve the dispute.

The appraisal process may also be initiated by the insurance company if they believe there is a need for an independent assessment of the loss or damage. This can occur when the insurer questions the validity or extent of the claim, or if there is a disagreement between the insurer and the policyholder.

Once the appraisal process is initiated, both parties typically select an appraiser to represent their interests. These appraisers then work together to reach a mutually agreeable resolution. If the appraisers are unable to reach a resolution, they may then select a neutral umpire to make a final decision.

| – The appraisal process is initiated when there is a dispute regarding the amount of loss or damage covered under an insurance policy. |

| – It can be initiated by either the policyholder or the insurance company. |

| – Appraisers are selected by both parties to represent their interests during the process. |

| – If the appraisers cannot reach a resolution, a neutral umpire may be selected to make a final decision. |

By understanding when and how the appraisal process is initiated, both insurers and policyholders can better navigate the sometimes complex world of insurance claims and come to a fair and impartial resolution.

Role of Appraisers in the Process

In the appraisal process, appraisers play a crucial role in demystifying the claims. They are responsible for assessing the value of the property or assets that have been damaged or lost in an insurance claim.

The primary role of appraisers is to determine the accurate and fair value of the property or assets. This helps in settling the claim in a fair and equitable manner. Appraisers utilize their expertise and knowledge of the industry to evaluate the damages and provide an objective assessment.

During the appraisal process, the appraisers from both the insurance company and the insured party work together to evaluate the damages. They may visit the site of the loss, examine the relevant documents, and gather any additional information necessary for an accurate appraisal.

Once the appraisal is complete, the appraisers present their findings and submit a written report. This report includes details about the property or assets, the extent of the damages, and the estimated value of the losses. The appraisers use their expertise to ensure that the report is comprehensive and unbiased.

The role of appraisers is vital in ensuring a fair and efficient resolution of insurance claims. Their objective assessment helps in determining the appropriate compensation for the losses and facilitates the process of claim settlement for both insurance companies and policyholders.

| – Assessing the value of damaged or lost property/assets |

| – Conducting site visits and examining relevant documents |

| – Gathering additional information for an accurate appraisal |

| – Collaborating with appraisers from insurance companies and insured parties |

| – Presenting findings and submitting comprehensive written reports |

How to Choose Appraisers for Your Claim?

When it comes to insurance claims, the appraisal process can often be mystifying, making it crucial to have the right appraisers on your side. Choosing the right appraisers is essential for a fair and accurate assessment of your claim. Here are some factors to consider when selecting appraisers:

| Experience and Qualifications | Look for appraisers who have experience specifically in insurance claims and are knowledgeable about the appraisal process. They should have a good understanding of the industry and be able to navigate through complex claims effectively. |

| Independence and Impartiality | It is important that the appraisers you choose are independent and impartial. They should not have any conflict of interest or bias towards any party involved in the claim. This ensures that the appraisal process remains fair and unbiased. |

| Professional Reputation | Do some research to find out about the appraisers’ professional reputation. Check for reviews or testimonials from previous clients to see if they have a track record of providing quality and reliable appraisals. A good reputation is a strong indicator of their competence and reliability. |

| Availability and Responsiveness | Make sure the appraisers you choose are available to handle your claim in a timely manner. They should be responsive to your inquiries and update you regularly on the progress of the appraisal. This ensures that your claim is processed efficiently and without unnecessary delays. |

| Cost | Consider the cost of the appraisers’ services and compare it with their qualifications and reputation. While it is important to find appraisers within your budget, remember that quality and expertise should be prioritized over cost. A thorough and accurate appraisal can greatly impact the outcome of your claim. |

By considering these factors, you can choose appraisers who will best represent your interests and ensure a fair and accurate assessment of your insurance claim. Remember, the appraisal process is crucial in determining the outcome of your claim, so it is important to choose appraisers wisely.

Understanding the Appraisal Clause

Demystifying the appraisal process in insurance claims involves understanding the appraisal clause. The appraisal clause is a provision in many insurance policies that allows the insured and the insurance company to resolve disputes over the value of a loss.

The appraisal process begins when the insured and the insurance company cannot agree on the value of the damages incurred. This can happen when there is a disagreement over the extent of the loss or the cost of repairs. In such cases, the appraisal clause provides a mechanism for an impartial third party, known as the appraiser, to determine the value of the loss.

| The insured selects an appraiser, the insurance company selects an appraiser, and these two appraisers work together to determine the value of the loss. |

| If the appraisers cannot agree, they appoint an umpire, who acts as an arbitrator and makes a final determination on the value of the loss. |

| The decision reached through the appraisal process is binding on both parties and becomes part of the insurance policy. |

The appraisal clause is designed to provide a fair and efficient method for resolving disputes over the value of a loss. It avoids the need for costly and time-consuming litigation, allowing both the insured and the insurance company to move forward and settle the claim.

Understanding the appraisal clause is essential for policyholders and insurance professionals alike. It ensures a clear understanding of the process and can help facilitate prompt and fair resolution of insurance claims.

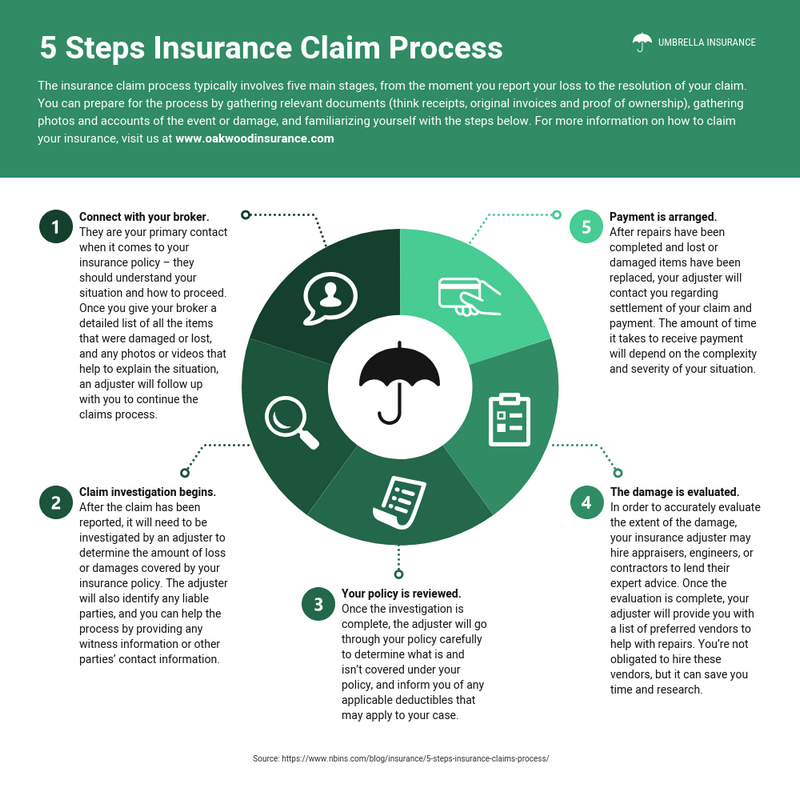

Steps Involved in the Appraisal Process

Demystifying the appraisal process in insurance claims involves understanding the steps involved. Here are the key steps:

- Notification: The first step is for the insured party to notify their insurance company about the loss or event that requires appraisal. This notification should include all relevant details of the claim.

- Assignment: Once the notification is received, the insurance company will assign an appraiser to assess the damage and determine the value of the claim. The appraiser is usually an independent third party.

- Inspection: The appraiser will then conduct an inspection of the property or item in question to assess the extent of the damage and gather evidence for the claim.

- Evidence Collection: During the inspection, the appraiser will collect all necessary evidence, such as photographs, videos, and documents, to support the appraisal process.

- Estimate: Based on the collected evidence, the appraiser will determine the cost of repair or replacement, considering factors like depreciation and current market value.

- Review: The appraiser’s estimate will be reviewed by the insurance company, who may request additional documentation or clarification if needed.

- Resolution: Once the review process is complete, the insurance company will provide the insured party with a final resolution, which may include the approved amount for the claim.

- Payment: If the claim is approved, the insurance company will issue payment to the insured party according to the terms of the insurance policy.

- Appeals: In case the insured party disagrees with the appraisal or the claim is denied, they may have the option to appeal the decision and provide additional evidence or arguments to support their case.

Understanding these steps can help insured parties navigate the insurance appraisal process more effectively and ensure a fair resolution to their claims.

Documentation Required for Appraisal

In the process of appraisal, documentation plays a crucial role in demystifying the complexity involved in insurance claims. The following documents are required to ensure a fair and comprehensive appraisal:

1. Insurance Policy: The policy documentation is essential to determine the coverage and limits of the insurance policy. It outlines the terms and conditions that apply to the claim.

2. Proof of Loss: This document is completed by the policyholder and provides a detailed account of the damages or losses incurred. It should include a description of the damage, estimated costs of repairs, and any supporting evidence such as photographs or receipts.

3. Estimates: It is important to provide several estimates from qualified contractors or repair professionals. These estimates should detail the scope of work, materials required, and associated costs.

4. Repair Receipts and Invoices: Any repair receipts or invoices related to the claim should be provided as supporting documentation. These documents validate the costs incurred during the repair process.

5. Incident Reports: If the claim is related to an accident or incident, it is essential to include any incident reports filed with the appropriate authorities or any other relevant documentation.

6. Medical Records: In the case of an injury claim, medical records such as doctor’s reports, hospital bills, and treatment plans should be submitted along with the claim.

7. Appraisal Agreement: An appraisal agreement is required in some cases, outlining the terms and conditions of the appraisal process. This document should be signed by both the policyholder and the insurance company.

Providing complete and accurate documentation is essential to facilitate a smooth and fair appraisal process. Failing to provide the necessary documentation may result in delays or complications in the resolution of the insurance claim.

How to Prepare for the Appraisal Inspection?

Demystifying the insurance appraisal process is crucial for policyholders to understand how their claims are determined. This comprehensive guide aims to explain the various steps involved in the appraisal process to empower individuals with the necessary knowledge. One critical step in the process is the appraisal inspection. This inspection is a key factor in determining the value of the insurance claim.

Preparing for the appraisal inspection is essential to ensure that all necessary information is available for the appraiser to make an accurate assessment. Here are some important steps to consider:

- Gather all relevant documentation: Before the appraisal inspection, collect all the relevant documents related to your insurance claim. This can include policy paperwork, previous repair estimates, photographs of damaged property, and any other supporting documentation that can help establish the value of your claim.

- Make a list of damages: Take the time to inspect your property thoroughly and make a detailed list of all damages. Be as specific as possible, noting the type of damage, its location, and any other relevant details. This will ensure that you don’t miss any damages during the appraisal inspection.

- Organize your evidence: In addition to gathering documents, organize your evidence in a clear and accessible manner. This could include creating a folder or digital file where all the relevant information and photographs are stored. Clear organization will make it easier for both you and the appraiser to navigate through the evidence during the inspection.

- Prepare for questions: During the appraisal inspection, the appraiser may ask you questions regarding the damages and the history of your property. Be prepared to answer these questions and provide any additional information that may be necessary. Having a clear understanding of the events leading up to the damage can help ensure that your claim is properly evaluated.

- Be present during the inspection: While it may not always be required, it is highly recommended that you be present during the appraisal inspection. This will allow you to provide any necessary explanations and clarify any uncertainties that the appraiser may have. Being present also ensures that the appraiser has access to all areas of your property that need to be inspected.

By following these steps and adequately preparing for the appraisal inspection, you can help ensure that your insurance claim accurately reflects the value of your damages. Remember to communicate openly with the appraiser, provide any necessary information, and be proactive in advocating for your rights as a policyholder.

Appraisal Hearing: What to Expect?

When it comes to insurance claims, the appraisal process can often seem confusing and overwhelming. However, understanding what to expect during an appraisal hearing can help demystify the process and ensure a smoother experience.

First and foremost, it’s important to remember that an appraisal hearing is a crucial step in the insurance claims process. This is where the two parties involved – the policyholder and the insurance company – present their arguments and evidence regarding the claim.

The purpose of the appraisal hearing is to resolve any disputes or disagreements between the policyholder and the insurance company regarding the value of the claim. Each party will have the opportunity to provide their own estimate and evidence supporting their position.

During the hearing, it’s important to be prepared and organized. This includes gathering all relevant documentation, such as the policy, receipts, photographs, and any other supporting evidence. It’s also crucial to clearly present your arguments and evidence in a concise and persuasive manner.

It’s important to note that the appraisal hearing is not a formal court proceeding. It’s generally less formal and less adversarial, with a neutral appraiser or panel of appraisers overseeing the process. The appraiser(s) will review the evidence presented by both parties and make a determination on the value of the claim.

It’s also important to be aware that the appraisal hearing is not necessarily the final step in the claims process. If either party is dissatisfied with the outcome, they may have the option to pursue other avenues, such as mediation or litigation.

In conclusion, understanding what to expect during an appraisal hearing can help policyholders navigate the claims process more effectively. Remember to be prepared, organized, and persuasive in presenting your arguments and evidence. And remember that the appraisal hearing is just one step in the overall insurance claims process.

Appraisal Process vs. Mediation

In the insurance industry, the appraisal process and mediation are both utilized to resolve disputes between policyholders and insurance companies. While they both aim to facilitate an agreement, there are key differences between the two.

The appraisal process is an alternative dispute resolution method used to determine the value of a claim. It involves an independent appraiser who assesses the damages and calculates a fair and unbiased settlement amount. This process is typically initiated when there is a disagreement between the insured and the insurer regarding the value of a claim. The appraisers appointed by each side review the evidence and present their findings to an umpire, who makes the final decision.

On the other hand, mediation is a voluntary process that involves a neutral third party, the mediator, who assists the parties in reaching a mutually acceptable resolution. Unlike the appraisal process, mediation focuses on facilitating communication and negotiation rather than providing a binding decision. The mediator helps identify common interests and assists in creating a solution that satisfies both parties.

While both the appraisal process and mediation can be effective in resolving insurance claim disputes, there are factors to consider when deciding which method to pursue. The appraisal process provides a more structured and formal approach, with an umpire making a binding decision based on the appraisers’ findings. In contrast, mediation offers more flexibility and opportunities for compromise, as the parties have greater control over the outcome.

Ultimately, the choice between the appraisal process and mediation depends on the specific circumstances of the dispute and the preferences of the parties involved. It is important for policyholders and insurance companies to understand the differences between these two methods in order to make informed decisions and effectively navigate the claims process.

Challenging the Appraisal Decision

In the process of claims adjustment, understanding and demystifying the appraisal process is essential. However, there may be instances where a policyholder disagrees with the outcome of the appraisal decision. In such cases, challenging the appraisal decision becomes necessary.

Here are some steps to follow when challenging an appraisal decision:

- Review the Appraisal Clause: Begin by carefully reviewing the appraisal clause in your insurance policy. This clause outlines the procedures and guidelines for the appraisal process and may provide information on how to challenge the decision.

- Consult with an Attorney: If you believe that the appraisal decision was unfair or incorrect, it may be helpful to consult with an attorney who specializes in insurance claims. They can review your case and provide guidance on the best course of action.

- Document Discrepancies: Gather all relevant documentation, including the initial claim, any supporting evidence, and the appraisal decision. Look for discrepancies or errors that may have affected the outcome of the appraisal.

- File an Appeal: Following the procedures outlined in your insurance policy, file an appeal with your insurance company. This typically involves submitting a letter stating your reasons for challenging the decision and providing any supporting documentation.

- Seek Mediation or Arbitration: If the appeal is unsuccessful or if the insurance company refuses to reconsider the decision, you may opt for mediation or arbitration. These alternative dispute resolution processes can help resolve the disagreement without resorting to litigation.

- Consider Legal Action: If all else fails, and you still believe that the appraisal decision was unjust, you may consider filing a lawsuit against the insurance company. Discuss this option with your attorney, as it can be a complex and lengthy process.

Challenging an appraisal decision requires careful preparation and adherence to the guidelines set forth in your insurance policy. By following these steps, you can effectively advocate for yourself and seek a fair resolution to your claim.

undefined

What is the appraisal process in insurance claims?

The appraisal process in insurance claims is a method of resolving disputes between insurance companies and policyholders regarding the value of a claim. It involves the appointment of a neutral third-party appraiser who assesses the damage and determines the appropriate amount of compensation.

Who can be an appraiser in the appraisal process?

An appraiser in the appraisal process can be a professional with expertise in assessing damages, such as a licensed contractor, engineer, or a professional with specialized knowledge in a specific field related to the claim.

What happens if the insurance company’s appraiser and the policyholder’s appraiser cannot agree?

If the insurance company’s appraiser and the policyholder’s appraiser cannot agree on the value of the claim, they will often select a neutral umpire. The umpire will review the evidence presented by both appraisers and make a final decision to determine the amount of compensation.

Is the decision made by the appraisers binding?

Yes, in most cases, the decision made by the appraisers is binding and cannot be appealed. It is a final resolution to the dispute regarding the value of the claim.

How long does the appraisal process typically take?

The duration of the appraisal process can vary depending on the complexity of the claim and the availability of the appraisers. However, it generally takes between a few weeks to a couple of months to complete.